)

How does an Aussie or Kiwi startup make a breakthrough in the US? In this article, Lucy Tan lays out a way for founders to frame those initial decisions.

Many Aussie and Kiwi startups inevitably face the challenge of breaking into a new market – and often, the logical next market is the US. While the US is often perceived as the holy grail due to the sheer size of the opportunity, it is also a market with:

- More competitors, with significant war chests of capital deployed into sales and marketing

- Higher-cost talent that is competitive to attract

- State-by-state peculiarities, such that each state can often feel like a new market in itself

So, how does an Aussie or Kiwi startup make a breakthrough in the US? In this article, I lay out a way for founders to frame those initial decisions: 1) when to break into the US market? 2) how to break into the US market? Some startups will decide to tackle Europe or APAC, but for the scope of this article, we’ll focus on the startups that decide the US is their ultimate market.

These learnings are synthesised from two sources: speaking with over 20 US venture capital funds (VCs) in the last two weeks, during which I spent time in both the San Francisco and New York startup ecosystems and the playbooks used by the giants in our ecosystem (e.g. Atlassian, Xero, Canva, Afterpay).

1. When to break into the US market

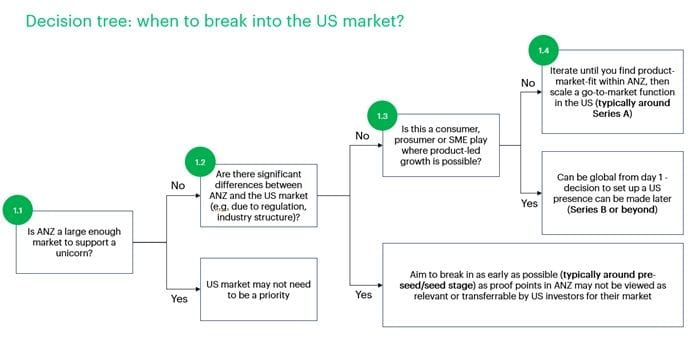

1.1 Is Australia or New Zealand (ANZ) a large enough market to support a unicorn?

If the ANZ market is large enough to support a unicorn, there may never be a need to go to the US. For example, Athena (a Square Peg portfolio company) is tackling Australia’s $100B mortgage market as a digital mortgage lender – when it comes to home ownership and mortgages, Australia is more than a large enough market!

But for the vast majority of ANZ startups, that won’t be the case.

1.2 Are there significant differences between ANZ and the US market?

If there are significant differences between the ANZ and US markets (e.g. you’re in a highly regulated industry, and the regulatory regime is very different by country), going as early as possible (pre-seed/seed) will likely be the right long-term decision.

The starkest example is startups building in business-to-business (B2B( healthcare. The US healthtech VCs I spoke to hold the view that any product-market fit (“PMF”) in ANZ does not necessarily translate in the US, given the vastly different systems around government rebates, insurers, and healthcare networks. Founders can fall into the trap of presenting great traction within ANZ, not knowing that it won’t be material to a US VC's investment decision.

1.3 Is this a consumer/prosumer/SME play where product-led growth is possible?

Let’s assume that the buyer, the value proposition and the structure of the market have some similarities between ANZ and the US. In this case, ANZ has a strong history of success with product-led growth (“PLG”) motions typically in consumer/prosumer/SME areas – these startups are typically global from day one and can afford to make the decision to set up a US presence later in their journey. For example:

- Canva didn’t open a US office until 2020, seven years post launch. By this time, it already had 40m monthly active users around the world, having grown with the rise of social media

- Atlassian had a false start in 2004 (3 years post founding), setting up a small New York office only to close it when they realised it wasn’t necessary. Atlassian had made their products self-serve, able to be purchased by developers from anywhere and grow virally within teams

1.4 Is this a mid-market/enterprise play where a sales-led motion is needed?

If a PLG motion is not possible and your startup needs to set up a sales function to go after midmarket or enterprise, that gives rise to a different set of considerations. Here, the most nuanced views I heard from US VCs were: if you’re at seed stage and trying to find PMF, it is often cheaper and easier to do that within your local market.

Coming to the US too early has several drawbacks: 1) it’s not necessarily going to help you find PMF any faster, and 2) US hires are comparatively more expensive—it's easy to burn a lot of capital before you even find PMF. Under that logic, the best pathway could be to find PMF in ANZ, then scale into the US aggressively by the time you reach Series A.

The trap for founders is having unrealistic expectations around whether your Series A can attract US investor attention. If only a tiny proportion of your revenue is in the US at this stage, this wouldn’t necessarily meet the bar for the vast majority of US VCs I spoke to. US VCs typically want to see material traction in their market or at least a pace of growth that suggests the revenue mix is quickly shifting towards the US. If you find yourself in this scenario where there are only small green shoots of growth from the US, the best pathway may be to raise from a local VC with a sizeable fund that can provide firepower to scale into the US and a track record of having supported startups breaking into that market.

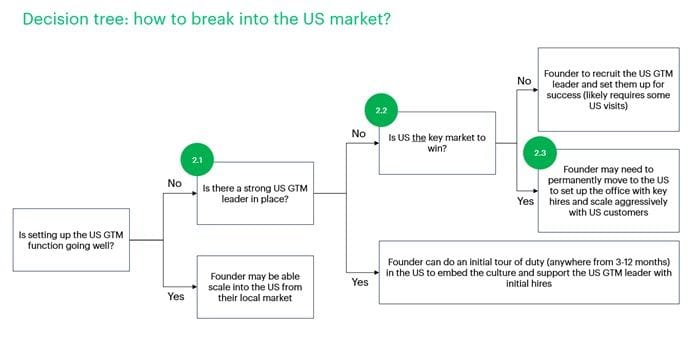

2. How to break into the US market?

In this section, I focus on startups that are targeting mid-market/enterprise with a sales-led motion. There are many different paths to success, so I wouldn’t treat any of the following as gospel – founders need to make their own calculus around the tradeoffs they’re willing to make and the constraints within which they must work.

2.1 Is there a strong US GTM (go-to-market) leader in place?

If your initial US market entry is not going well, you wouldn’t be the exception to the rule. Even Xero, a massive success story from our part of the world, had trouble – they found that the US was so big it felt like shouting into a vacuum. It pushed their cost base up, and it was difficult to hire staff, given the far more competitive market. As a small challenger company with no brand awareness, they didn’t have the right to hire their dream team from day one.

The first thing you need to do is hire your initial US GTM team. Typically, the right composition is two account executives, and the sales leader found in parallel over 4-6 months. Xero’s method of finding this initial talent was to get out into industry events and conferences and ask relevant accountants/vendors who were the most urgent executives out there building a profile and demonstrating thought leadership. This initial set-up is critical – Xero suffered a high US executive turnover in the early years, which took a lot of momentum out of their US GTM efforts. In that time, Quickbooks (the dominant competitor in the US) was able to respond quickly with its own cloud product.

2.2 Is the US the key market to win?

The degree to which the founder needs to be in the US for the above process is entirely dependent on the situation, but a good rule of thumb is: if things are not going well AND the US is the key market to win for your startup, the key lever the founder can pull is to spend more time in the US themselves.

The founder’s presence helps to 1) set up the key hires for success and 2) embed the startup's values and culture into the US team. The Atlassian founders noted that while they hired the first 50 people themselves, the next 50 were hired by others, and that group was not aligned with Atlassian’s work ethic and mission. This led the founders to codify the values explicitly.

2.3 “Go hard or go home” scaling

Once the initial US GTM team is in place, the overwhelming sentiment from US VCs was that you need to scale fast and aggressively. There are three main reasons for that:

- One underappreciated characteristic of the US market is that buyers within midmarket and enterprise are a lot more willing to respond to a cold outreach and try the ‘hot new tool’. That means outbound efforts that may not be as effective in ANZ are likely to be effective over there

- Momentum compounds. Afterpay launched in the US in 2018 and quickly signed up marquee apparel brands like Urban Outfitters. Once you land a big customer, a snowball effect kicks in as that credibility helps to attract more logos

- The competitive intensity in the US market is high – having a great product is necessary but not sufficient. Distribution matters. Xero, for example, couldn’t compete with Quickbooks on marketing spend, so the accountant channel became a key method of distribution

If you have additional thoughts or learnings to share on this topic, I would love to hear from you. Please reach out to [email protected]

This article was originally published on Square Peg's blog, available here, and has been republished with permission.

)